Stablecoin Wars

Why Zelle, Western Union, and Venmo are all launching their own stablecoins

The most common retort I receive when explaining stablecoins is: “Why would I ever need to use stablecoins? Zelle and Venmo work great!”

I agree that Zelle and Venmo are great; I’m a power user of both. But, shouldn’t it then come as a surprise that not only Zelle and Venmo, but also Western Union are all exploring or launching stablecoins?

Stablecoins make real what payments have given the illusion of for a while: stablecoins help money move continuously and settle instantly, at low cost. With that in mind, can stablecoins improve upon the existing business models of these companies?

How does each work today

Zelle

Zelle is owned by a consortium of banks: JP Morgan Chase, Bank of America, Wells Fargo, Capital One, PNC, U.S. Bank, and Truist.

It’s easiest to think of Zelle as a messaging and settlement layer built on existing banking rails. When you “send” money through Zelle, you are not actually sending money from one Zelle account to another. Instead, you are just using Zelle to tell each bank to debit the sender’s account and credit the receiver’s account with the posted amount.

The actual settlement happens later through Zelle’s private interbank network and the Federal Reserve’s clearing system. Funds disappear and appear instantly for the users because the participating banks front the credit and assume that settlement will clear later.

Clearly, there are some limitations with this model:

Both sender and receiver must bank with a Zelle-member institution

Transfers are currently domestic-only, and limited to Zelle-partner banks (although there are many of these)

True settlement still depends on Fed interbank hours and batch settlement processes (it appears 24/7 but actually is not)

Zelle transfers can be expensive for banks, but they continue to support the system to keep money circulating inside the banking system, rather than flowing to fintech wallets. Zelle launched a few years after Venmo, but today does much more volume than any of its competitors.

Venmo

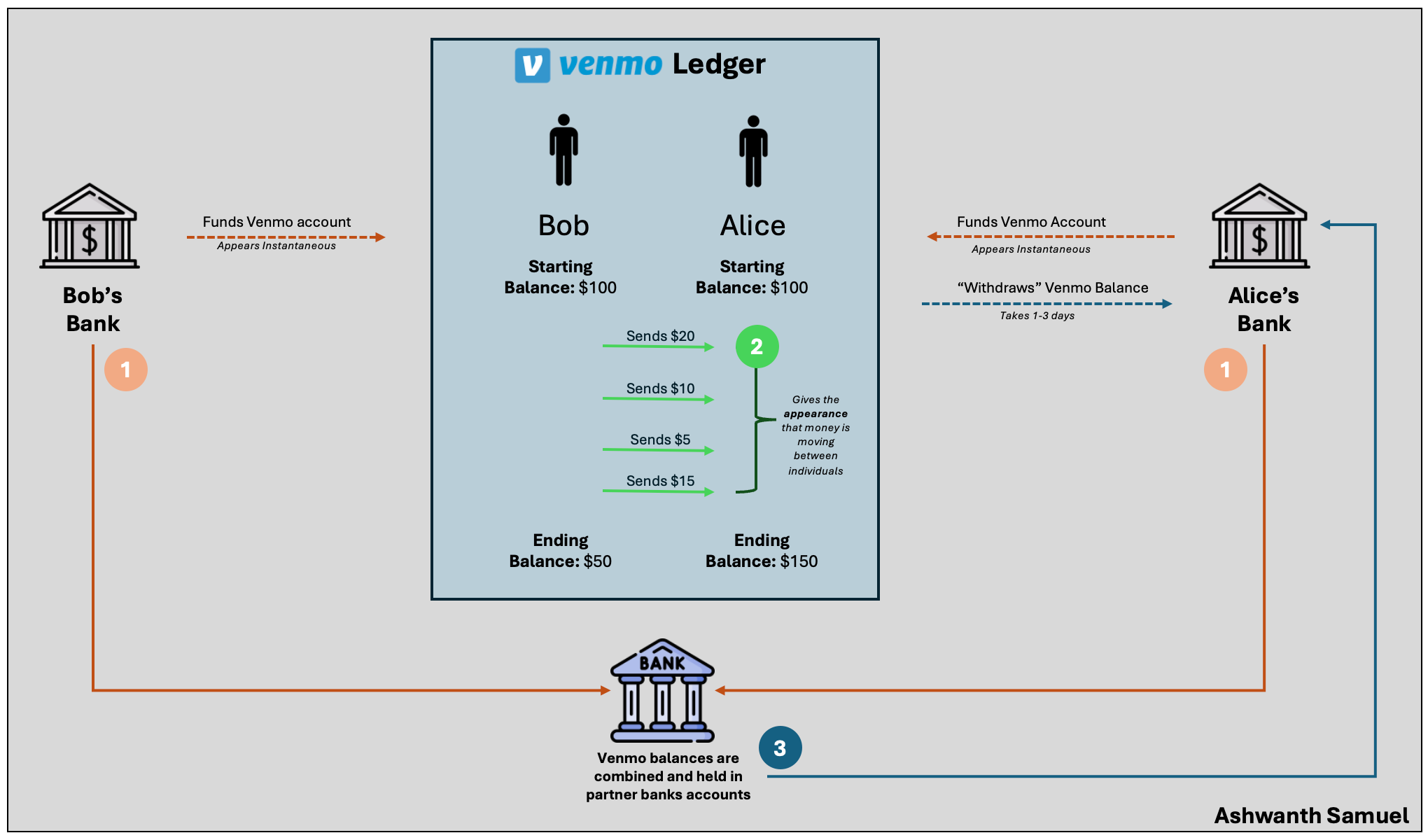

Venmo, owned by PayPal since 2013, functions as a digital wallet with an internal ledger. Once you add bank deposits to your Venmo and you accrue a balance, that money does not leave the Venmo/PayPal ecosystem until you decide to withdraw your funds.

When you send a friend money, Venmo simply updates balances on its own books; no bank money moves yet. This is another instance where the company, Venmo, fronts the credit so it looks instantaneous to the customers. If your Venmo balance is underfunded, Venmo is authorized to pull funds from your linked bank or card. This can take one to three days, because it requires Venmo to interact outside of its own ecosystem.

When users “cash out” of Venmo, they settle through ACH (slow, free) or card networks (instant, fee-based). This is because all user balances are pooled together at partner banks (i.e., your Venmo funds are lumped together with everyone else’s balances – see “Direct Deposit” in Venmo User Agreement).

Western Union

Western Union (WU) predates both fintech apps (and even the internet!). It is a global money transmitter, not a bank.

A sender can initiate a transfer online or at a local Western Union agent (think about those counters behind the checkout line at your local grocery store). Western Union collects the funds and provides a Money Transfer Control Number (MTCN). The recipient then redeems the money at a WU location or via bank deposit, sharing the MTCN for confirmation. To make payouts “instant,” WU pre-funds local agents worldwide; essentially WU fronts a ton of cash in order to make this system work. This exposes WU to:

FX risk, since cross-border settlements take a long time to occur, long enough for currencies to appreciate/depreciate

Counterparty risk, with 400K agents around the world.

Operational burdens, because every payout depends on banks and local partners

The main issues

All three models create the appearance of instant payment but in reality lack settlement finality: the point at which a payment becomes irreversible, unconditional, and legally settled.

I believe this illusion creates three foundational risks:

Credit and Liquidity Risk for the companies that front money. If a payment fails or doesn’t come through, the company that fronted the money is left holding the bag.

Settlement delays create operational risk, especially when relying on so many counterparties. There are millions of unsettled transfers that must be reconciled every day.

Bad actors can take advantage of settlement lags. For example, attackers can send funds, receive goods, and then reverse or cancel the underlying bank transfer before the settlement actually clears. (see “Someone Pretends to Be Your Friend…” scam highlighted by Venmo).

How Stablecoins Could Fix the Weak Points

Stablecoins eliminate the settlement finality issue. Stablecoin tokens settle atomically, meaning that transfer and finality occur together, on-chain, without reliance on multiple rails, card networks or correspondent banks.

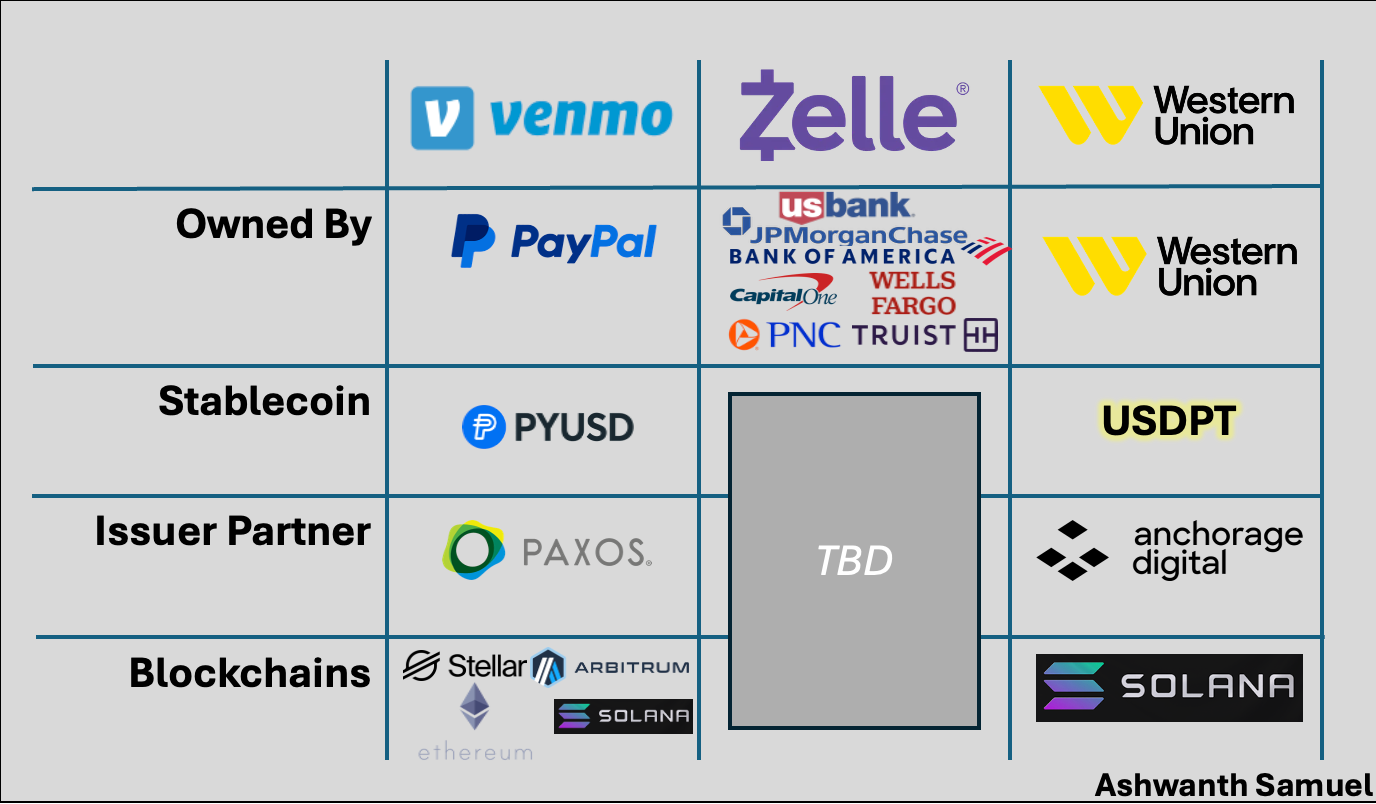

Zelle’s New Pilot

Early Warning Systems, Zelle’s ownership consortium, recently announced a stablecoin exploration effort. EWS/Zelle has not confirmed whether it will:

Issue a consortium-backed token

Integrate with existing stablecoins; or

Leverage bank-issued tokens on permissioned networks

Whatever path it takes, it is clear that Zelle is looking to expand its market share beyond just domestic payments and capture international flows without relying on correspondent banking.

Venmo’s PYUSD

PayPal launched its stablecoin, PYUSD in 2023, issued by Paxos Trust Company and backed 1:1 with cash and short-term Treasuries. Venmo users can hold PYUSD, send it to other Venmo users, or transfer it to other crypto wallet addresses. PYUSD lets PayPal/Venmo replace the slow, fee-heavy ACH layer with real-time, on-chain settlement.

In Venmo, I can hold PYUSD in my wallet and send it to anyone else on Venmo who has ‘accept crypto’ enabled. I can also send it to crypto addresses outside the PayPal ecosystem (like ashwanth.eth) for a small fee. Receiving or transferring crypto via other accounts on Venmo results in no fees.

Western Union’s USDPT

Western Union, the money transfer dinosaur, also announced the launch of the US Dollar Payment Token (USDPT) stablecoin on Solana, with Anchorage Digital as the regulated issuer.

For WU, the stablecoin represents the only realistic way to cut FX risk and pre-funding costs while maintaining compliance across borders. To me, it seems that the company is willingly cannibalizing its own high-fee model in exchange for scale and real-time global reach (a perfect example of the Innovator’s Dilemma!)

While all three companies are clearly interested in stablecoins, it’s unclear if the explorations are driven by a desire to reduce the settlement-lag / finality, better manage risk, or simply to take advantage of the sheer size and rapid growth of the international peer-to-peer (p2p) payments industry.

A lot of decisions remain before any of these companies actually launch or move forward with their stablecoin initiatives, although Venmo is furthest along. I’ve outlined a quick overview of each company’s progress so-far:

Are We Reaching Stablecoin Fatigue?

Honestly, probably. Every payment company now wants its own stablecoin. Fiserv even announced this summer that they have technology to let credit unions and regional banks launch and issue their own stablecoins… but is that actually useful?

Here’s when I think launching a stablecoin might be worth it from a payments use-case perspective:

Existing rails or methods are too slow or costly

The service does not require individuals to on-and-off ramp to/from fiat to stablecoins (i.e., people are fine with passing money around the Venmo platform)

You can ride the tailwind of increasing global transfers

You do a lot of business on the evenings or weekends

Settling in batches at the Fed causes you heartburn

The number of businesses that actually fit those criteria is small. For instance, I’m not sure St. Cloud Credit Union, a regional bank that announced its own stablecoin launch earlier this fall, checks many of those boxes.

And note that I’m only talking about stablecoins for payments. Others have made arguments about stablecoins for loyalty – where companies can use stablecoins to monetize retention and float – but I’ll have to explore this separate topic in a future post.

Stablecoins can help fix settlement lags, but most institutions don’t face this today. Institutions like Venmo, Zelle, and Western Union, however, could stand to gain from the efficiencies that stablecoins offer.